Predict Loan Repayment

Objective: Given historical data on loans given out with information on whether or not the borrower defaulted (charge-off), determine whether or not a borrower will pay back their loan.

Source: Udemy | Python for Data Science and Machine Learning Bootcamp

Data used in the below analysis: Subset of LendingClub DataSet from Kaggle.

Actual files used: Info | Data

#importing libraries to be used

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

%matplotlib inline

data_info = pd.read_csv('../DATA/lending_club_info.csv', index_col='LoanStatNew') #reading data desc

#created a function to get the desc of any column in our dataset

def feat_info(col_name):

print(data_info.loc[col_name]['Description'])

sns.set_style('whitegrid')

#reading data in DataFrame

df = pd.read_csv('../DATA/lending_club_loan_two.csv')

#Getting details of the data

df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 396030 entries, 0 to 396029

Data columns (total 27 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 loan_amnt 396030 non-null float64

1 term 396030 non-null object

2 int_rate 396030 non-null float64

3 installment 396030 non-null float64

4 grade 396030 non-null object

5 sub_grade 396030 non-null object

6 emp_title 373103 non-null object

7 emp_length 377729 non-null object

8 home_ownership 396030 non-null object

9 annual_inc 396030 non-null float64

10 verification_status 396030 non-null object

11 issue_d 396030 non-null object

12 loan_status 396030 non-null object

13 purpose 396030 non-null object

14 title 394275 non-null object

15 dti 396030 non-null float64

16 earliest_cr_line 396030 non-null object

17 open_acc 396030 non-null float64

18 pub_rec 396030 non-null float64

19 revol_bal 396030 non-null float64

20 revol_util 395754 non-null float64

21 total_acc 396030 non-null float64

22 initial_list_status 396030 non-null object

23 application_type 396030 non-null object

24 mort_acc 358235 non-null float64

25 pub_rec_bankruptcies 395495 non-null float64

26 address 396030 non-null object

dtypes: float64(12), object(15)

memory usage: 81.6+ MB

df.describe().transpose()

| count | mean | std | min | 25% | 50% | 75% | max | |

|---|---|---|---|---|---|---|---|---|

| loan_amnt | 396030.0 | 14113.888089 | 8357.441341 | 500.00 | 8000.00 | 12000.00 | 20000.00 | 40000.00 |

| int_rate | 396030.0 | 13.639400 | 4.472157 | 5.32 | 10.49 | 13.33 | 16.49 | 30.99 |

| installment | 396030.0 | 431.849698 | 250.727790 | 16.08 | 250.33 | 375.43 | 567.30 | 1533.81 |

| annual_inc | 396030.0 | 74203.175798 | 61637.621158 | 0.00 | 45000.00 | 64000.00 | 90000.00 | 8706582.00 |

| dti | 396030.0 | 17.379514 | 18.019092 | 0.00 | 11.28 | 16.91 | 22.98 | 9999.00 |

| open_acc | 396030.0 | 11.311153 | 5.137649 | 0.00 | 8.00 | 10.00 | 14.00 | 90.00 |

| pub_rec | 396030.0 | 0.178191 | 0.530671 | 0.00 | 0.00 | 0.00 | 0.00 | 86.00 |

| revol_bal | 396030.0 | 15844.539853 | 20591.836109 | 0.00 | 6025.00 | 11181.00 | 19620.00 | 1743266.00 |

| revol_util | 395754.0 | 53.791749 | 24.452193 | 0.00 | 35.80 | 54.80 | 72.90 | 892.30 |

| total_acc | 396030.0 | 25.414744 | 11.886991 | 2.00 | 17.00 | 24.00 | 32.00 | 151.00 |

| mort_acc | 358235.0 | 1.813991 | 2.147930 | 0.00 | 0.00 | 1.00 | 3.00 | 34.00 |

| pub_rec_bankruptcies | 395495.0 | 0.121648 | 0.356174 | 0.00 | 0.00 | 0.00 | 0.00 | 8.00 |

Starting with Exploratory Data Analysis!

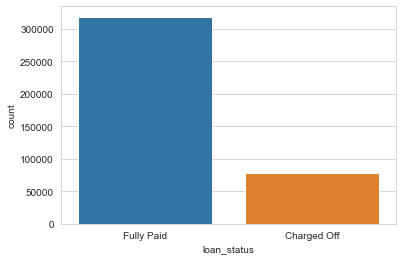

sns.countplot(x='loan_status',data=df)

Since we are trying to predict loan_status, the above plot makes it clear that our historic data is not well balanced. This means our model will not have a great precision / recall as data is unbalanced.

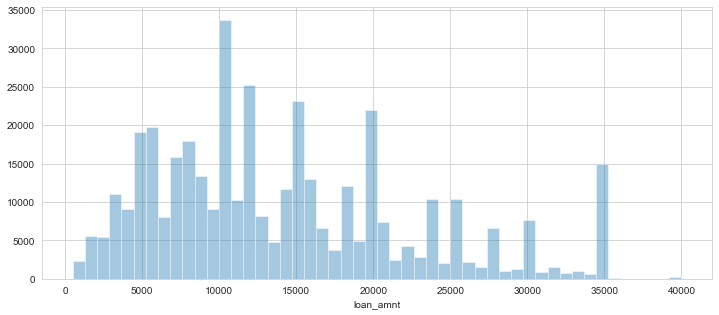

plt.figure(figsize=(12,5))

sns.distplot(df['loan_amnt'], bins=50, kde=False)

Most of the loan amounts is concentrated around 5000-20000 with very few values at 40000

#checking correlations among continuous features

df.corr()

| loan_amnt | int_rate | installment | annual_inc | dti | open_acc | pub_rec | revol_bal | revol_util | total_acc | mort_acc | pub_rec_bankruptcies | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| loan_amnt | 1.000000 | 0.168921 | 0.953929 | 0.336887 | 0.016636 | 0.198556 | -0.077779 | 0.328320 | 0.099911 | 0.223886 | 0.222315 | -0.106539 |

| int_rate | 0.168921 | 1.000000 | 0.162758 | -0.056771 | 0.079038 | 0.011649 | 0.060986 | -0.011280 | 0.293659 | -0.036404 | -0.082583 | 0.057450 |

| installment | 0.953929 | 0.162758 | 1.000000 | 0.330381 | 0.015786 | 0.188973 | -0.067892 | 0.316455 | 0.123915 | 0.202430 | 0.193694 | -0.098628 |

| annual_inc | 0.336887 | -0.056771 | 0.330381 | 1.000000 | -0.081685 | 0.136150 | -0.013720 | 0.299773 | 0.027871 | 0.193023 | 0.236320 | -0.050162 |

| dti | 0.016636 | 0.079038 | 0.015786 | -0.081685 | 1.000000 | 0.136181 | -0.017639 | 0.063571 | 0.088375 | 0.102128 | -0.025439 | -0.014558 |

| open_acc | 0.198556 | 0.011649 | 0.188973 | 0.136150 | 0.136181 | 1.000000 | -0.018392 | 0.221192 | -0.131420 | 0.680728 | 0.109205 | -0.027732 |

| pub_rec | -0.077779 | 0.060986 | -0.067892 | -0.013720 | -0.017639 | -0.018392 | 1.000000 | -0.101664 | -0.075910 | 0.019723 | 0.011552 | 0.699408 |

| revol_bal | 0.328320 | -0.011280 | 0.316455 | 0.299773 | 0.063571 | 0.221192 | -0.101664 | 1.000000 | 0.226346 | 0.191616 | 0.194925 | -0.124532 |

| revol_util | 0.099911 | 0.293659 | 0.123915 | 0.027871 | 0.088375 | -0.131420 | -0.075910 | 0.226346 | 1.000000 | -0.104273 | 0.007514 | -0.086751 |

| total_acc | 0.223886 | -0.036404 | 0.202430 | 0.193023 | 0.102128 | 0.680728 | 0.019723 | 0.191616 | -0.104273 | 1.000000 | 0.381072 | 0.042035 |

| mort_acc | 0.222315 | -0.082583 | 0.193694 | 0.236320 | -0.025439 | 0.109205 | 0.011552 | 0.194925 | 0.007514 | 0.381072 | 1.000000 | 0.027239 |

| pub_rec_bankruptcies | -0.106539 | 0.057450 | -0.098628 | -0.050162 | -0.014558 | -0.027732 | 0.699408 | -0.124532 | -0.086751 | 0.042035 | 0.027239 | 1.000000 |

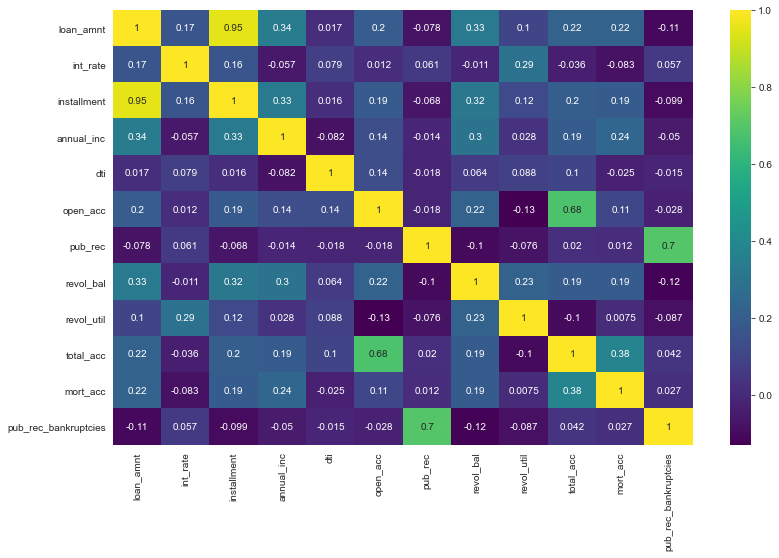

We can better visualize this with a heat map!

plt.figure(figsize=(13,8))

sns.heatmap(df.corr(), annot=True, cmap='viridis')

We can explore the high correlation of installment with loan amount. This is as per expectations as we know the amount of installment must depend on the loan taken.

feat_info('installment')

The monthly payment owed by the borrower if the loan originates.

feat_info('loan_amnt')

The listed amount of the loan applied for by the borrower. If at some point in time, the credit department reduces the loan amount, then it will be reflected in this value.

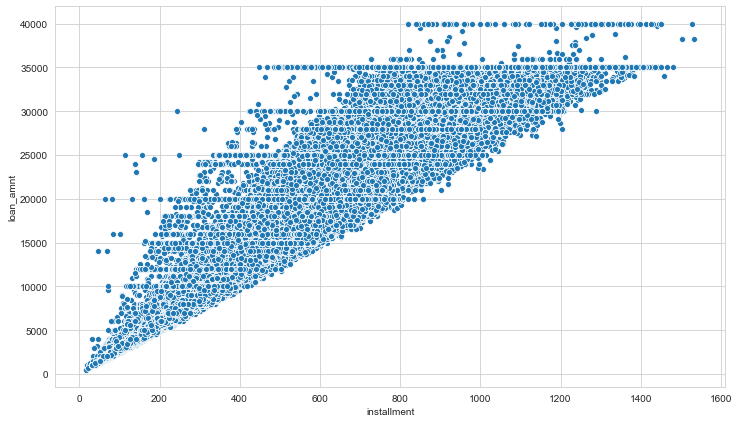

plt.figure(figsize=(12,7))

sns.scatterplot(x='installment',y='loan_amnt',data=df)

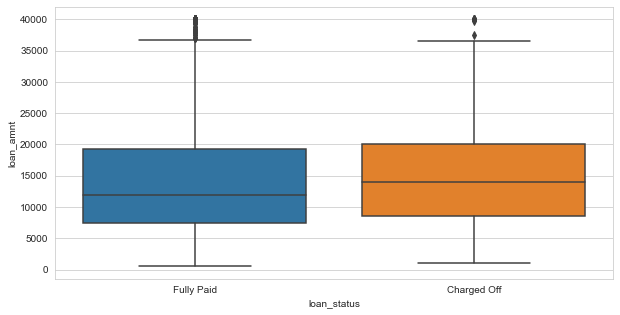

plt.figure(figsize=(10,5))

sns.boxplot(x='loan_status',y='loan_amnt',data=df)

df.groupby(by='loan_status')['loan_amnt'].describe()

| count | mean | std | min | 25% | 50% | 75% | max | |

|---|---|---|---|---|---|---|---|---|

| loan_status | ||||||||

| Charged Off | 77673.0 | 15126.300967 | 8505.090557 | 1000.0 | 8525.0 | 14000.0 | 20000.0 | 40000.0 |

| Fully Paid | 318357.0 | 13866.878771 | 8302.319699 | 500.0 | 7500.0 | 12000.0 | 19225.0 | 40000.0 |

df.columns

Index(['loan_amnt', 'term', 'int_rate', 'installment', 'grade', 'sub_grade',

'emp_title', 'emp_length', 'home_ownership', 'annual_inc',

'verification_status', 'issue_d', 'loan_status', 'purpose', 'title',

'dti', 'earliest_cr_line', 'open_acc', 'pub_rec', 'revol_bal',

'revol_util', 'total_acc', 'initial_list_status', 'application_type',

'mort_acc', 'pub_rec_bankruptcies', 'address'],

dtype='object')

df['grade'].unique()

array(['B', 'A', 'C', 'E', 'D', 'F', 'G'], dtype=object)

df['sub_grade'].unique()

array(['B4', 'B5', 'B3', 'A2', 'C5', 'C3', 'A1', 'B2', 'C1', 'A5', 'E4',

'A4', 'A3', 'D1', 'C2', 'B1', 'D3', 'D5', 'D2', 'E1', 'E2', 'E5',

'F4', 'E3', 'D4', 'G1', 'F5', 'G2', 'C4', 'F1', 'F3', 'G5', 'G4',

'F2', 'G3'], dtype=object)

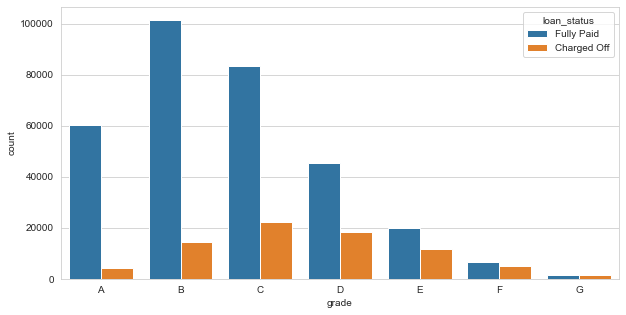

plt.figure(figsize=(10,5))

grade_sorted = sorted(df['grade'].unique())

sns.countplot(x='grade',data=df,hue='loan_status', order=grade_sorted)

plt.figure(figsize=(13,6))

sub_grade_sorted = sorted(df['sub_grade'].unique())

sns.countplot(x='sub_grade',data=df, order=sub_grade_sorted, palette = 'coolwarm')

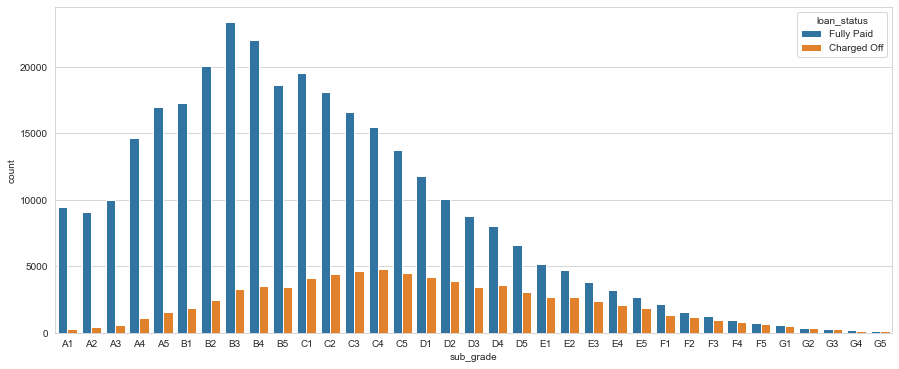

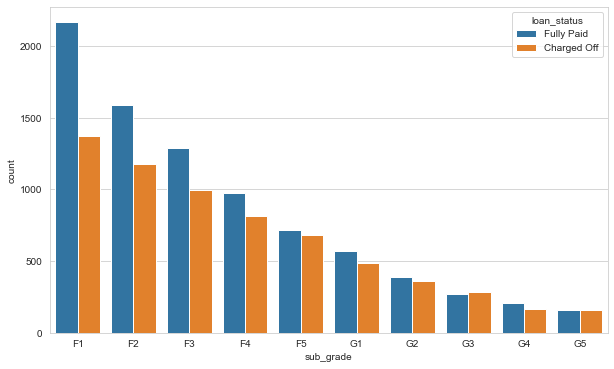

plt.figure(figsize=(15,6))

sub_grade_sorted = sorted(df['sub_grade'].unique())

sns.countplot(x='sub_grade',data=df, order=sub_grade_sorted, hue='loan_status')

It seems like F and G grade loans don’t get paid back often

plt.figure(figsize=(10,6))

df_grade_FG = df[(df['grade']=='F') | (df['grade'] == 'G')]

sub_grade_sorted = sorted(df_grade_FG['sub_grade'].unique())

sns.countplot(x='sub_grade', data = df_grade_FG, order = sub_grade_sorted, hue='loan_status')

def loan_status(string):

if string == 'Fully Paid':

return 1

else:

return 0

df['loan_repaid'] = df['loan_status'].apply(loan_status)

df.head()

| loan_amnt | term | int_rate | installment | grade | sub_grade | emp_title | emp_length | home_ownership | annual_inc | ... | pub_rec | revol_bal | revol_util | total_acc | initial_list_status | application_type | mort_acc | pub_rec_bankruptcies | address | loan_repaid | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 10000.0 | 36 months | 11.44 | 329.48 | B | B4 | Marketing | 10+ years | RENT | 117000.0 | ... | 0.0 | 36369.0 | 41.8 | 25.0 | w | INDIVIDUAL | 0.0 | 0.0 | 0174 Michelle Gateway\nMendozaberg, OK 22690 | 1 |

| 1 | 8000.0 | 36 months | 11.99 | 265.68 | B | B5 | Credit analyst | 4 years | MORTGAGE | 65000.0 | ... | 0.0 | 20131.0 | 53.3 | 27.0 | f | INDIVIDUAL | 3.0 | 0.0 | 1076 Carney Fort Apt. 347\nLoganmouth, SD 05113 | 1 |

| 2 | 15600.0 | 36 months | 10.49 | 506.97 | B | B3 | Statistician | < 1 year | RENT | 43057.0 | ... | 0.0 | 11987.0 | 92.2 | 26.0 | f | INDIVIDUAL | 0.0 | 0.0 | 87025 Mark Dale Apt. 269\nNew Sabrina, WV 05113 | 1 |

| 3 | 7200.0 | 36 months | 6.49 | 220.65 | A | A2 | Client Advocate | 6 years | RENT | 54000.0 | ... | 0.0 | 5472.0 | 21.5 | 13.0 | f | INDIVIDUAL | 0.0 | 0.0 | 823 Reid Ford\nDelacruzside, MA 00813 | 1 |

| 4 | 24375.0 | 60 months | 17.27 | 609.33 | C | C5 | Destiny Management Inc. | 9 years | MORTGAGE | 55000.0 | ... | 0.0 | 24584.0 | 69.8 | 43.0 | f | INDIVIDUAL | 1.0 | 0.0 | 679 Luna Roads\nGreggshire, VA 11650 | 0 |

5 rows × 28 columns

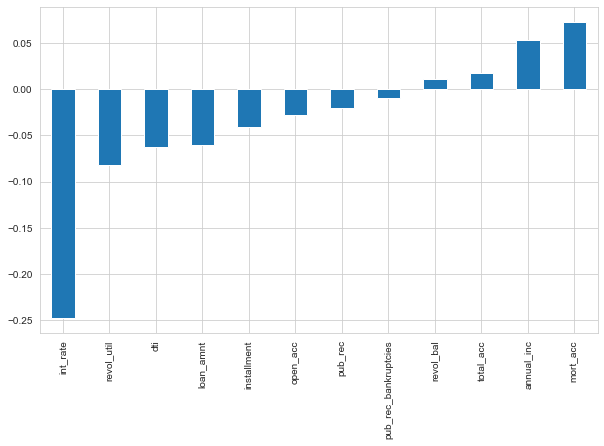

plt.figure(figsize=(10,6))

df.corr()['loan_repaid'].sort_values().drop('loan_repaid').plot(kind='bar')

The loan repayment is most correlated with annual_inc and mort_acc and highly uncorrelated with interest rate.

print("annual_inc:")

feat_info('annual_inc')

print('mort_acc:')

feat_info('mort_acc')

print('int_rate:')

feat_info('int_rate')

annual_inc:

The self-reported annual income provided by the borrower during registration.

mort_acc:

Number of mortgage accounts.

int_rate:

Interest Rate on the loan

Data PreProcessing!

We need to fill missing data or remove unnecessary features and convert categorical features into numerical ones using dummy variable (one hot encoding)

df.shape[0] #number of entries in our data

396030

df.isnull().sum()

loan_amnt 0

term 0

int_rate 0

installment 0

grade 0

sub_grade 0

emp_title 22927

emp_length 18301

home_ownership 0

annual_inc 0

verification_status 0

issue_d 0

loan_status 0

purpose 0

title 1755

dti 0

earliest_cr_line 0

open_acc 0

pub_rec 0

revol_bal 0

revol_util 276

total_acc 0

initial_list_status 0

application_type 0

mort_acc 37795

pub_rec_bankruptcies 535

address 0

loan_repaid 0

dtype: int64

#convert into % of total data frame

df.isnull().sum()/df.shape[0]

loan_amnt 0.000000

term 0.000000

int_rate 0.000000

installment 0.000000

grade 0.000000

sub_grade 0.000000

emp_title 0.057892

emp_length 0.046211

home_ownership 0.000000

annual_inc 0.000000

verification_status 0.000000

issue_d 0.000000

loan_status 0.000000

purpose 0.000000

title 0.004431

dti 0.000000

earliest_cr_line 0.000000

open_acc 0.000000

pub_rec 0.000000

revol_bal 0.000000

revol_util 0.000697

total_acc 0.000000

initial_list_status 0.000000

application_type 0.000000

mort_acc 0.095435

pub_rec_bankruptcies 0.001351

address 0.000000

loan_repaid 0.000000

dtype: float64

We need to keep/remove features with missing values. Let’s determine that one by one.

print("emp_title:")

feat_info('emp_title')

print("emp_length:")

feat_info('emp_length')

emp_title:

The job title supplied by the Borrower when applying for the loan.*

emp_length:

Employment length in years. Possible values are between 0 and 10 where 0 means less than one year and 10 means ten or more years.

df['emp_title'].nunique()

173105

df['emp_title'].value_counts()

Teacher 4389

Manager 4250

Registered Nurse 1856

RN 1846

Supervisor 1830

...

Color tech 1

New York City Department of Education 1

Bartender/Food Server 1

Commercial Ara Executive 1

El Cortez Hotel & Casino 1

Name: emp_title, Length: 173105, dtype: int64

There are way too many unique titles to convert them into dummy variable, we shall drop it

df.drop('emp_title', axis=1, inplace=True)

sorted(df['emp_length'].dropna().unique())

['1 year',

'10+ years',

'2 years',

'3 years',

'4 years',

'5 years',

'6 years',

'7 years',

'8 years',

'9 years',

'< 1 year']

emp_length_order = [ '< 1 year',

'1 year',

'2 years',

'3 years',

'4 years',

'5 years',

'6 years',

'7 years',

'8 years',

'9 years',

'10+ years']

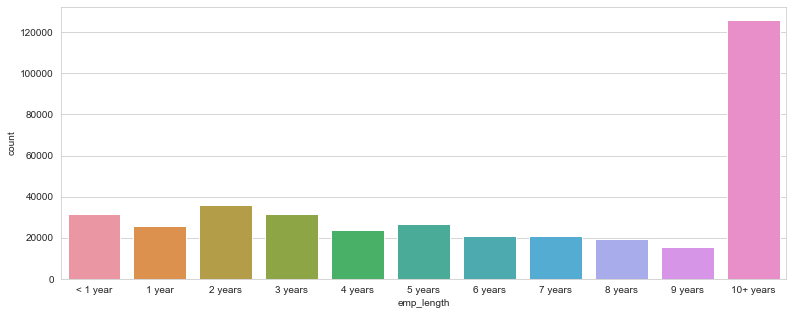

plt.figure(figsize=(13,5))

sns.countplot(x='emp_length',data=df,order=emp_length_order)

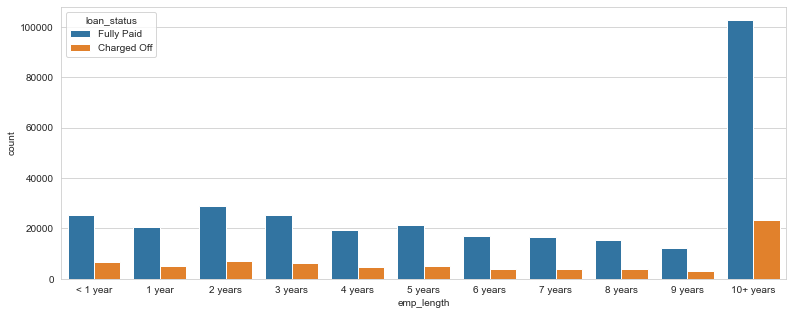

plt.figure(figsize=(13,5))

sns.countplot(x='emp_length',data=df,order=emp_length_order, hue='loan_status')

This doesn’t really inform us if there is a strong relationship between employment length and being charged off, we need a percentage of charge offs per category or what percent of people per employment category didn’t pay back their loan.

data_for_emp_len = df[df['loan_repaid']==1].groupby(by='emp_length').count()

data_for_emp_len = pd.merge(data_for_emp_len,

pd.DataFrame(df.groupby(by='emp_length').count()

['loan_repaid']).reset_index(),on = 'emp_length')

data_for_emp_len['percentage'] = data_for_emp_len['loan_repaid_x'] / data_for_emp_len['loan_repaid_y']

data_for_emp_len.set_index('emp_length',inplace=True)

data_for_emp_len

| loan_amnt | term | int_rate | installment | grade | sub_grade | home_ownership | annual_inc | verification_status | issue_d | ... | revol_util | total_acc | initial_list_status | application_type | mort_acc | pub_rec_bankruptcies | address | loan_repaid_x | loan_repaid_y | percentage | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| emp_length | |||||||||||||||||||||

| 1 year | 20728 | 20728 | 20728 | 20728 | 20728 | 20728 | 20728 | 20728 | 20728 | 20728 | ... | 20712 | 20728 | 20728 | 20728 | 18126 | 20666 | 20728 | 20728 | 25882 | 0.800865 |

| 10+ years | 102826 | 102826 | 102826 | 102826 | 102826 | 102826 | 102826 | 102826 | 102826 | 102826 | ... | 102766 | 102826 | 102826 | 102826 | 95511 | 102753 | 102826 | 102826 | 126041 | 0.815814 |

| 2 years | 28903 | 28903 | 28903 | 28903 | 28903 | 28903 | 28903 | 28903 | 28903 | 28903 | ... | 28886 | 28903 | 28903 | 28903 | 25355 | 28848 | 28903 | 28903 | 35827 | 0.806738 |

| 3 years | 25483 | 25483 | 25483 | 25483 | 25483 | 25483 | 25483 | 25483 | 25483 | 25483 | ... | 25468 | 25483 | 25483 | 25483 | 22220 | 25437 | 25483 | 25483 | 31665 | 0.804769 |

| 4 years | 19344 | 19344 | 19344 | 19344 | 19344 | 19344 | 19344 | 19344 | 19344 | 19344 | ... | 19333 | 19344 | 19344 | 19344 | 16526 | 19321 | 19344 | 19344 | 23952 | 0.807615 |

| 5 years | 21403 | 21403 | 21403 | 21403 | 21403 | 21403 | 21403 | 21403 | 21403 | 21403 | ... | 21391 | 21403 | 21403 | 21403 | 18691 | 21381 | 21403 | 21403 | 26495 | 0.807813 |

| 6 years | 16898 | 16898 | 16898 | 16898 | 16898 | 16898 | 16898 | 16898 | 16898 | 16898 | ... | 16884 | 16898 | 16898 | 16898 | 15002 | 16878 | 16898 | 16898 | 20841 | 0.810806 |

| 7 years | 16764 | 16764 | 16764 | 16764 | 16764 | 16764 | 16764 | 16764 | 16764 | 16764 | ... | 16747 | 16764 | 16764 | 16764 | 15284 | 16751 | 16764 | 16764 | 20819 | 0.805226 |

| 8 years | 15339 | 15339 | 15339 | 15339 | 15339 | 15339 | 15339 | 15339 | 15339 | 15339 | ... | 15327 | 15339 | 15339 | 15339 | 14142 | 15323 | 15339 | 15339 | 19168 | 0.800240 |

| 9 years | 12244 | 12244 | 12244 | 12244 | 12244 | 12244 | 12244 | 12244 | 12244 | 12244 | ... | 12235 | 12244 | 12244 | 12244 | 11192 | 12233 | 12244 | 12244 | 15314 | 0.799530 |

| < 1 year | 25162 | 25162 | 25162 | 25162 | 25162 | 25162 | 25162 | 25162 | 25162 | 25162 | ... | 25139 | 25162 | 25162 | 25162 | 21629 | 25055 | 25162 | 25162 | 31725 | 0.793128 |

11 rows × 28 columns

plt.figure(figsize=(13,5))

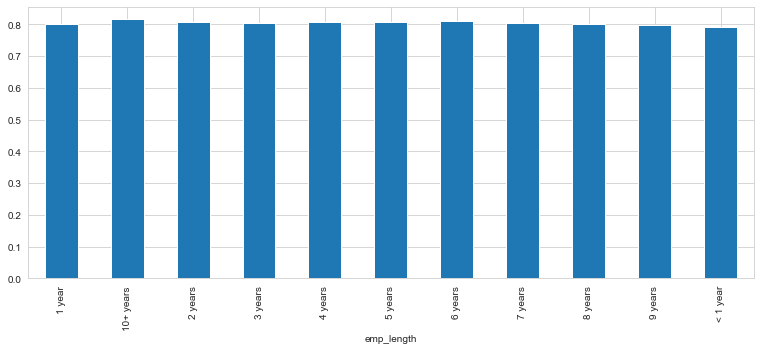

data_for_emp_len['percentage'].plot(kind='bar')

The above plot shows % of poeple who paid their loans from the total number of people who took loan grouped at employee length. We can see that this is extremely same across all emp_lengths so we can drop the same.

df.drop('emp_length',axis=1,inplace=True)

df.isnull().sum()

loan_amnt 0

term 0

int_rate 0

installment 0

grade 0

sub_grade 0

home_ownership 0

annual_inc 0

verification_status 0

issue_d 0

loan_status 0

purpose 0

title 1755

dti 0

earliest_cr_line 0

open_acc 0

pub_rec 0

revol_bal 0

revol_util 276

total_acc 0

initial_list_status 0

application_type 0

mort_acc 37795

pub_rec_bankruptcies 535

address 0

loan_repaid 0

dtype: int64

print("purpose:")

feat_info('purpose')

print("title:")

feat_info('title')

purpose:

A category provided by the borrower for the loan request.

title:

The loan title provided by the borrower

df['purpose'].unique()

array(['vacation', 'debt_consolidation', 'credit_card',

'home_improvement', 'small_business', 'major_purchase', 'other',

'medical', 'wedding', 'car', 'moving', 'house', 'educational',

'renewable_energy'], dtype=object)

df['title'].unique()

array(['Vacation', 'Debt consolidation', 'Credit card refinancing', ...,

'Credit buster ', 'Loanforpayoff', 'Toxic Debt Payoff'],

dtype=object)

The title is just a sub category for purpose, we can drop it!

df.drop('title', axis=1, inplace=True)

df['mort_acc'].value_counts()

0.0 139777

1.0 60416

2.0 49948

3.0 38049

4.0 27887

5.0 18194

6.0 11069

7.0 6052

8.0 3121

9.0 1656

10.0 865

11.0 479

12.0 264

13.0 146

14.0 107

15.0 61

16.0 37

17.0 22

18.0 18

19.0 15

20.0 13

24.0 10

22.0 7

21.0 4

25.0 4

27.0 3

23.0 2

32.0 2

26.0 2

31.0 2

30.0 1

28.0 1

34.0 1

Name: mort_acc, dtype: int64

There are many ways we could deal with this missing data. Build a simple model to fill it in, fill it in based on the mean of the other columns, or bin the columns into categories and then set NaN as its own category.

df.corr()['mort_acc'].sort_values()

int_rate -0.082583

dti -0.025439

revol_util 0.007514

pub_rec 0.011552

pub_rec_bankruptcies 0.027239

loan_repaid 0.073111

open_acc 0.109205

installment 0.193694

revol_bal 0.194925

loan_amnt 0.222315

annual_inc 0.236320

total_acc 0.381072

mort_acc 1.000000

Name: mort_acc, dtype: float64

The column mort_acc is most correlated with total_acc.

mean_mort_total = df.groupby(by='total_acc').mean()['mort_acc']

mean_mort_total

total_acc

2.0 0.000000

3.0 0.052023

4.0 0.066743

5.0 0.103289

6.0 0.151293

...

124.0 1.000000

129.0 1.000000

135.0 3.000000

150.0 2.000000

151.0 0.000000

Name: mort_acc, Length: 118, dtype: float64

We’ll try to fill the missing values using this series

def fill_mort_acc(total,mort):

if np.isnan(mort):

return mean_mort_total[total]

else:

return mort

df['mort_acc'] = df.apply(lambda x : fill_mort_acc(x['total_acc'],x['mort_acc']), axis=1)

df.isnull().sum()/df.shape[0]

loan_amnt 0.000000

term 0.000000

int_rate 0.000000

installment 0.000000

grade 0.000000

sub_grade 0.000000

home_ownership 0.000000

annual_inc 0.000000

verification_status 0.000000

issue_d 0.000000

loan_status 0.000000

purpose 0.000000

dti 0.000000

earliest_cr_line 0.000000

open_acc 0.000000

pub_rec 0.000000

revol_bal 0.000000

revol_util 0.000697

total_acc 0.000000

initial_list_status 0.000000

application_type 0.000000

mort_acc 0.000000

pub_rec_bankruptcies 0.001351

address 0.000000

loan_repaid 0.000000

dtype: float64

As the data covered by revol_util and pub_rec_bankruptcies account for less than 0.05% of the data, we’ll drop these.

df.drop('revol_util',axis=1,inplace=True)

df.drop('pub_rec_bankruptcies',axis=1,inplace=True)

df.isnull().sum()

loan_amnt 0

term 0

int_rate 0

installment 0

grade 0

sub_grade 0

home_ownership 0

annual_inc 0

verification_status 0

issue_d 0

loan_status 0

purpose 0

dti 0

earliest_cr_line 0

open_acc 0

pub_rec 0

revol_bal 0

total_acc 0

initial_list_status 0

application_type 0

mort_acc 0

address 0

loan_repaid 0

dtype: int64

Convert categorical data into dummy variables

#getting textual columns

df.select_dtypes(include='object').columns

Index(['term', 'grade', 'sub_grade', 'home_ownership', 'verification_status',

'issue_d', 'loan_status', 'purpose', 'earliest_cr_line',

'initial_list_status', 'application_type', 'address'],

dtype='object')

feat_info('term')

The number of payments on the loan. Values are in months and can be either 36 or 60.

df['term'].unique()

array([' 36 months', ' 60 months'], dtype=object)

def term_change(string):

if string == ' 36 months':

return 36

else:

return 60

df['term'] = df['term'].apply(term_change)

df['term'].unique()

array([36, 60])

Since grade is a part of sub_grade, we can drop it!

df.drop('grade',axis=1,inplace=True)

#converting sub grade into dummy variables

dummy_df = pd.get_dummies(df,columns=['sub_grade'],drop_first=True)

dummy_df.select_dtypes(include='object').columns

Index(['home_ownership', 'verification_status', 'issue_d', 'loan_status',

'purpose', 'earliest_cr_line', 'initial_list_status',

'application_type', 'address'],

dtype='object')

features = ['verification_status', 'application_type','initial_list_status','purpose']

dummy_df = pd.get_dummies(dummy_df,columns=features,drop_first=True)

dummy_df.columns

Index(['loan_amnt', 'term', 'int_rate', 'installment', 'home_ownership',

'annual_inc', 'issue_d', 'loan_status', 'dti', 'earliest_cr_line',

'open_acc', 'pub_rec', 'revol_bal', 'total_acc', 'mort_acc', 'address',

'loan_repaid', 'sub_grade_A2', 'sub_grade_A3', 'sub_grade_A4',

'sub_grade_A5', 'sub_grade_B1', 'sub_grade_B2', 'sub_grade_B3',

'sub_grade_B4', 'sub_grade_B5', 'sub_grade_C1', 'sub_grade_C2',

'sub_grade_C3', 'sub_grade_C4', 'sub_grade_C5', 'sub_grade_D1',

'sub_grade_D2', 'sub_grade_D3', 'sub_grade_D4', 'sub_grade_D5',

'sub_grade_E1', 'sub_grade_E2', 'sub_grade_E3', 'sub_grade_E4',

'sub_grade_E5', 'sub_grade_F1', 'sub_grade_F2', 'sub_grade_F3',

'sub_grade_F4', 'sub_grade_F5', 'sub_grade_G1', 'sub_grade_G2',

'sub_grade_G3', 'sub_grade_G4', 'sub_grade_G5',

'verification_status_Source Verified', 'verification_status_Verified',

'application_type_INDIVIDUAL', 'application_type_JOINT',

'initial_list_status_w', 'purpose_credit_card',

'purpose_debt_consolidation', 'purpose_educational',

'purpose_home_improvement', 'purpose_house', 'purpose_major_purchase',

'purpose_medical', 'purpose_moving', 'purpose_other',

'purpose_renewable_energy', 'purpose_small_business',

'purpose_vacation', 'purpose_wedding'],

dtype='object')

dummy_df.select_dtypes(include='object').columns

Index(['home_ownership', 'issue_d', 'loan_status', 'earliest_cr_line',

'address'],

dtype='object')

dummy_df['home_ownership'].value_counts()

MORTGAGE 198348

RENT 159790

OWN 37746

OTHER 112

NONE 31

ANY 3

Name: home_ownership, dtype: int64

def home_owner(string):

if string == 'NONE' or string == 'ANY':

return 'OTHER'

else:

return string

dummy_df['home_ownership'] = dummy_df['home_ownership'].apply(home_owner)

dummy_df['home_ownership'].value_counts()

MORTGAGE 198348

RENT 159790

OWN 37746

OTHER 146

Name: home_ownership, dtype: int64

dummy_df = pd.get_dummies(dummy_df,columns=['home_ownership'],drop_first=True)

dummy_df.select_dtypes(include='object').columns

Index(['issue_d', 'loan_status', 'earliest_cr_line', 'address'], dtype='object')

dummy_df['address'] = dummy_df['address'].apply(lambda x : x[-5:])

dummy_df['address']

0 22690

1 05113

2 05113

3 00813

4 11650

...

396025 30723

396026 05113

396027 70466

396028 29597

396029 48052

Name: address, Length: 396030, dtype: object

dummy_df = pd.get_dummies(dummy_df,columns=['address'],drop_first=True)

dummy_df.columns

Index(['loan_amnt', 'term', 'int_rate', 'installment', 'annual_inc', 'issue_d',

'loan_status', 'dti', 'earliest_cr_line', 'open_acc', 'pub_rec',

'revol_bal', 'total_acc', 'mort_acc', 'loan_repaid', 'sub_grade_A2',

'sub_grade_A3', 'sub_grade_A4', 'sub_grade_A5', 'sub_grade_B1',

'sub_grade_B2', 'sub_grade_B3', 'sub_grade_B4', 'sub_grade_B5',

'sub_grade_C1', 'sub_grade_C2', 'sub_grade_C3', 'sub_grade_C4',

'sub_grade_C5', 'sub_grade_D1', 'sub_grade_D2', 'sub_grade_D3',

'sub_grade_D4', 'sub_grade_D5', 'sub_grade_E1', 'sub_grade_E2',

'sub_grade_E3', 'sub_grade_E4', 'sub_grade_E5', 'sub_grade_F1',

'sub_grade_F2', 'sub_grade_F3', 'sub_grade_F4', 'sub_grade_F5',

'sub_grade_G1', 'sub_grade_G2', 'sub_grade_G3', 'sub_grade_G4',

'sub_grade_G5', 'verification_status_Source Verified',

'verification_status_Verified', 'application_type_INDIVIDUAL',

'application_type_JOINT', 'initial_list_status_w',

'purpose_credit_card', 'purpose_debt_consolidation',

'purpose_educational', 'purpose_home_improvement', 'purpose_house',

'purpose_major_purchase', 'purpose_medical', 'purpose_moving',

'purpose_other', 'purpose_renewable_energy', 'purpose_small_business',

'purpose_vacation', 'purpose_wedding', 'home_ownership_OTHER',

'home_ownership_OWN', 'home_ownership_RENT', 'address_05113',

'address_11650', 'address_22690', 'address_29597', 'address_30723',

'address_48052', 'address_70466', 'address_86630', 'address_93700'],

dtype='object')

#drop issue_d as we shouldn't know beforehand whether loadn would be issued or now

dummy_df.drop('issue_d',axis=1,inplace=True)

feat_info('earliest_cr_line')

The month the borrower's earliest reported credit line was opened

dummy_df['earliest_cr_line'] = dummy_df['earliest_cr_line'].apply(lambda x : int(x[-4:]))

dummy_df['earliest_cr_line']

0 1990

1 2004

2 2007

3 2006

4 1999

...

396025 2004

396026 2006

396027 1997

396028 1990

396029 1998

Name: earliest_cr_line, Length: 396030, dtype: int64

dummy_df.select_dtypes(include='object').columns

Index(['loan_status'], dtype='object')

We can now start with Model building!

from sklearn.model_selection import train_test_split

dummy_df.drop('loan_status',axis=1,inplace=True) #we alreday have loan_repaid in 0 and 1

X = dummy_df.drop('loan_repaid',axis=1).values

y = dummy_df['loan_repaid'].values

from sklearn.preprocessing import MinMaxScaler

X_train,X_test,y_train, y_test = train_test_split(X,y,random_state=101,test_size=0.2)

scale = MinMaxScaler()

X_train = scale.fit_transform(X_train)

X_test = scale.transform(X_test)

import tensorflow as tf

from tensorflow.keras.models import Sequential

from tensorflow.keras.layers import Dense,Dropout

from tensorflow.keras.optimizers import Adam

X_train.shape

(316824, 76)

We are creating a Sequential Model, with activation function as Rectified Linear Unit, with a Dropout layer of 20% neurons switching off, sigmoid function as activation for output. Since its a binary classification problem, we are using Binary Cross-Entropy as loss function and Adam as optimizer.

model = Sequential()

model.add(Dense(units=76, activation='relu'))

model.add(Dropout(0.2))

model.add(Dense(units=38,activation='relu'))

model.add(Dropout(0.2))

model.add(Dense(units=19,activation='relu'))

model.add(Dropout(0.2))

model.add(Dense(units=1,activation='sigmoid'))

model.compile(loss='binary_crossentropy', optimizer='adam')

model.fit(X_train,y_train,batch_size=256,epochs=50,validation_data=(X_test,y_test),

verbose=1)

Epoch 1/50

1238/1238 [==============================] - 2s 2ms/step - loss: 0.3007 - val_loss: 0.2633

Epoch 2/50

1238/1238 [==============================] - 2s 2ms/step - loss: 0.2664 - val_loss: 0.2604

Epoch 3/50

1238/1238 [==============================] - 2s 2ms/step - loss: 0.2637 - val_loss: 0.2597

Epoch 4/50

1238/1238 [==============================] - 2s 2ms/step - loss: 0.2626 - val_loss: 0.2592

Epoch 5/50

1238/1238 [==============================] - 2s 2ms/step - loss: 0.2618 - val_loss: 0.2591

Epoch 6/50

1238/1238 [==============================] - 2s 2ms/step - loss: 0.2612 - val_loss: 0.2593

.

.

.

Epoch 50/50

1238/1238 [==============================] - 3s 2ms/step - loss: 0.2549 - val_loss: 0.2575

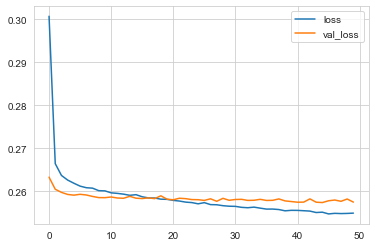

loss = pd.DataFrame(model.history.history)

loss.plot()

The model is overfitting. We can try to fix that using Early stopping. We can even play around with dropout layers.

from tensorflow.keras.callbacks import EarlyStopping

early_stop = EarlyStopping(monitor='val_loss', mode='min', verbose=1, patience=5)

n_model = Sequential()

n_model.add(Dense(units=76, activation='relu'))

n_model.add(Dropout(0.2))

n_model.add(Dense(units=38,activation='relu'))

n_model.add(Dropout(0.2))

n_model.add(Dense(units=19,activation='relu'))

n_model.add(Dropout(0.2))

n_model.add(Dense(units=1,activation='sigmoid'))

n_model.compile(loss='binary_crossentropy', optimizer='adam')

n_model.fit(X_train,y_train,batch_size=256,epochs=50,validation_data=(X_test,y_test),

verbose=1, callbacks = [early_stop])

Epoch 1/50

1238/1238 [==============================] - 3s 2ms/step - loss: 0.3013 - val_loss: 0.2625

Epoch 2/50

1238/1238 [==============================] - 3s 2ms/step - loss: 0.2666 - val_loss: 0.2607

Epoch 3/50

1238/1238 [==============================] - 4s 3ms/step - loss: 0.2639 - val_loss: 0.2593

Epoch 4/50

1238/1238 [==============================] - 3s 3ms/step - loss: 0.2630 - val_loss: 0.2593

Epoch 5/50

1238/1238 [==============================] - 3s 2ms/step - loss: 0.2618 - val_loss: 0.2594

Epoch 6/50

1238/1238 [==============================] - 3s 2ms/step - loss: 0.2614 - val_loss: 0.2589

Epoch 7/50

.

.

.

Epoch 21/50

1238/1238 [==============================] - 3s 2ms/step - loss: 0.2580 - val_loss: 0.2587

Epoch 00021: early stopping

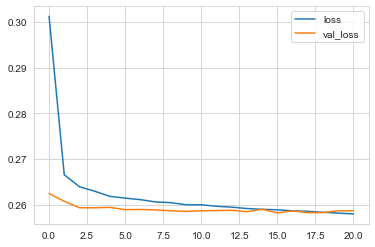

loss = pd.DataFrame(n_model.history.history)

loss.plot()

Evaluate the model

from sklearn.metrics import classification_report, confusion_matrix

n_predictions = n_model.predict_classes(X_test)

print(confusion_matrix(y_test,n_predictions))

[[ 6840 8653]

[ 114 63599]]

print(classification_report(y_test,n_predictions))

precision recall f1-score support

0 0.98 0.44 0.61 15493

1 0.88 1.00 0.94 63713

accuracy 0.89 79206

macro avg 0.93 0.72 0.77 79206

weighted avg 0.90 0.89 0.87 79206

Predicting a new entry

import random

random.seed(101)

random_ind = random.randint(0,len(df))

new_customer = dummy_df.drop('loan_repaid',axis=1).iloc[random_ind]

new_customer

loan_amnt 24000.00

term 60.00

int_rate 13.11

installment 547.43

annual_inc 85000.00

...

address_30723 0.00

address_48052 0.00

address_70466 0.00

address_86630 0.00

address_93700 0.00

Name: 304691, Length: 76, dtype: float64

new_customer = scale.transform(new_customer.values.reshape(1,76))

n_model.predict_classes(new_customer)

array([[1]], dtype=int32)

We’ve predicted that we would give this person the loan. Let’s check if they returned it.

dummy_df.iloc[random_ind]['loan_repaid']

1.0